Neven Zitek

Neven Zitek As a part of my job-related responsibilities, I’ve performed many IT due diligence analyses for customers, and one of the biggest problems I’ve encountered was identifying customers’ true IT costs. You’d imagine the process would be as simple as asking the finance department and acquiring accounting information, and you’d be right. But, the problems start once you get the answers:

“Servers……4pcs,” “Computer licenses……78pcs,” “Assorted IT equipment……7pcs.” Wait… what?

“There might be some more; however, if some (non-IT) department requested IT hardware / software, than it gets accounted for in their cost center, and we have no way of identifying it as IT-related cost.” This is the most typical answer I’d get.

If your organization handles the accounting of IT equipment in the same manner, I’m guessing you have your own, parallel system (or Excel sheet) in which you track IT and IT-related costs. I admit, even I had one of these at one point.

Cost classification and identification

Accounting within ITIL Financial Management differs a lot from “traditional” accounting, in the sense that we need additional cost categories and characteristics defined in order to enable identification and tracking of service-oriented expenses. The result of the service-oriented accounting function is greater and more detailed understanding regarding service costs, which is extremely valuable for provisioning and consumption information, and planning.

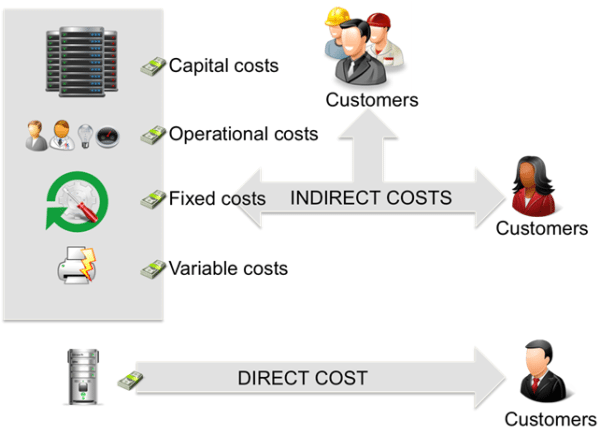

Figure 1: ITIL cost classification

Figure 1: ITIL cost classification

In order to achieve effective IT accounting, you must be able to assign all cost entries to appropriate services. Depending on the services you provide, and their complexity, you’ll define appropriate granularity of the sub-service components. This task belongs to the Service recording function, which should be able to translate and assign costs to appropriate services or sub-services.

Some higher-level expense categories, known as Cost types, such as hardware, software, personnel, accommodation, etc., should be defined as well, as those attributes are valuable for reporting and analysis, and they are presented in commonly used financial terms.

What you also need to understand are the Cost classifications – which designate the end purpose of the cost. As shown in Figure 1, we classify costs as:

- Capital costs – purchases that carry residual value (reduced via depreciation); e.g., hardware, facility infrastructure for hosting equipment, etc.

- Operational costs – day-to-day recurring expenses – costs of running the IT operations; e.g., salaries, electric bill, hardware maintenance, rentals, etc.

- Direct costs – cost of providing IT service that can be allocated to a specific customer, and is consumed by that customer alone; e.g., extra server for HR software, with licenses.

- Indirect costs – when providing IT services, most of the resources are shared (hardware network, IT staff) among end-users or customers. Those shared costs have to be divided fairly among end-users or customers by fair breakdown, e.g., per LAN port in the case of networking service. A common problem among the Type III IT organizations is the unused portion of the service, which contributes to overhead. What should you do when the unused portion becomes used – should you charge for it, or not? This would be a good time to read Branimir’s post ITIL Financial Management – To charge or not to charge?, if you haven’t already.

- Fixed costs – predictable costs that don’t vary over time, or with service usage; e.g., replacing end-of-life hardware, lease contracts, etc.

- Variable costs – costs that vary over time or with service usage; e.g., licenses per user, energy, or in the case of printing – how much you use a printer will affect amount of paper and toner cartridge used.

Some like to present Cost classification as: Capital vs. Operational, Direct vs. Indirect, and Fixed vs. Variable, but personally, I believe that such presentation may be confusing, as it suggests that those classes exclude each other. In normal IT operation you have a fair mixture of cost classes; for example, the HR department will share indirect costs for networking service with the rest of the company, but will also receive direct cost regarding any specific service (e.g., extra server for HR software) exclusive to the HR department.

What do accountants do for fun?

As IT accounting processes and practices mature and become service oriented, we gather more evidence about the performance of the IT organization. This information becomes visible through translating cost account data into service account information, enabling a higher level of service strategy development or execution.

You can start improving by asking yourself few simple questions: Is current accounting software capable of creating and managing needed subcategories and classes? Are current personnel capable of accurately recording IT-related costs? And, are you going to use the data as intended? From my experience, the most difficult and error-prone task was accurate recording of IT-related costs. You can try to solve this problem by improving the internal ordering process, so extra information about the cost type, class, service, etc. is recorded and matches the records in the accounting software. Of course, you could become an accountant yourself; I hear that accountants add up the telephone books for fun :).

To implement ISO 20000 easily and efficiently, use our ISO 20000 Documentation Toolkit that provides step-by-step guidance for full ISO 20000 compliance.